India’s Insurance Moment Has Arrived

- Jul 9

- 5 min read

Article Summary

India’s insurance market is booming, but true protection still lags behind. This article reveals the real gap between premium growth and actual coverage. With insurtech acceleration, embedded protection, faster claims and micro-insurance, the next decade belongs to platforms that deliver depth, trust and access - not just sales.

Author: Dr Kavindra Kumar Singh, CTO, SMC Insurance Brokers Pvt Ltd

India’s Insurance Moment Has Arrived

Now, the Question is whether we will Build Depth and not Just Scale

India is often described as one of the fastest-growing insurance markets in the world. The premiums are rising. Digital adoption is spreading. Insurtech is attracting capital and talent. And yet, step away from the dashboards and into everyday life - one truth becomes unavoidable. India is still dramatically underinsured.

This gap between rapid industry growth and weak real-world protection is structural. And at the same time, it is also fixable.

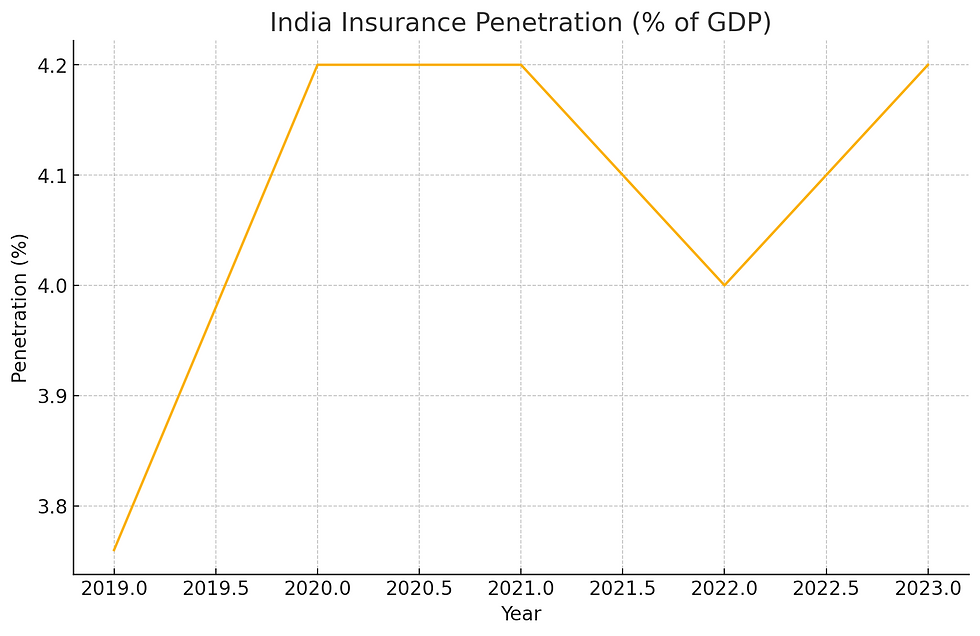

Growth Is Real - Penetration Is Not

India’s insurance premiums continue to climb, but penetration tells a more sobering story.

According to the IRDAI Annual Report 2023-24:

Total insurance penetration declined to 3.7% of GDP.

Life insurance penetration fell to 2.8%.

Non-life insurance stayed near 1.0%.

This matters because penetration measures how deeply insurance is woven into the economy, not how loudly it is sold.

Insurance Penetration in India (% of GDP, FY2019-FY2024)

Despite economic growth, insurance has failed to keep pace. In contrast:

Global insurance penetration averages ~7%.

In advanced economies, it often exceeds 9-11%.

(Source: Swiss Re Sigma)

India is growing, but insurance is not yet growing with India.

Density Tells the Same Story

Insurance density reflects how much protection an average citizen actually buys.

As per IRDAI and Swiss Re data:

India’s insurance density in FY 2023-24 stood at ~USD 95 per capita.

Global average density exceeds USD 850.

This is a signal that risk protection has not yet become a lived habit for most Indians.

The Coverage Gap Is Widest Where Risk Is Highest

The problem becomes sharper when viewed through geography. Multiple government and World Bank-linked studies show:

Urban India: ~60-65% of households have at least one insurance policy.

Rural India: Fewer than 25-30% households are meaningfully insured.

(Source: World Bank, NITI Aayog, IRDAI-backed studies)

This is not due to lack of awareness alone. Rural and informal households face:

Irregular income

Seasonal risk

Higher exposure to health and climate shocks

Yet most products assume fixed salaries, long commitments, and paperwork-heavy journeys. India’s risk profile changed. But unfortunately, insurance design did not.

The Good News - Insurtech Is Scaling Fast

Technology is clearly transforming the industry. As per IMARC Group:

India’s Insurtech market was valued at USD 0.9 billion in 2024 and is projected to reach USD 11.9 billion by 2033. It predicts a CAGR of over 29%.

This growth is driven by:

Smartphone penetration beyond metros

Digital payments becoming default

API-driven insurer integrations

AI-enabled underwriting and fraud detection

For the first time, distribution is no longer the biggest bottleneck. But speed without direction can widen the gap it hopes to close.

The Shift Ahead: From Selling Policies to Selling Protection

The next phase of India’s insurance journey will not be defined by more products. It will be defined by better timing, relevance, and trust.

Insurance Will Move Closer To Daily Life

This is because insurance works best when it appears at the right moment. Embedded insurance models are already proving effective like:

Motor cover at vehicle purchase

Health cover bundled with credit

Travel and accident cover linked to mobility and commerce

This removes fear and reduces decision fatigue. Global studies suggest embedded insurance can increase first-time adoption by 20-30%.

(Source: Swiss Re Institute)

Data Will Replace Guesswork

India’s diversity makes old underwriting models blunt and exclusionary. Thus, insurers and platforms are now using:

Transaction behaviour

Occupation and mobility signals

Device and payment data

This allows risk to be priced fairly instead of conservatively. While clearly protecting insurers, it also brings the excluded into the system.

Claims Will Become The Real Brand

Historically, trust was built at sale. But gradually, it is now shifting to claim settlement. According to IRDAI:

Faster claim settlement is the strongest driver of renewal intent.

Transparency matters more than premium discounts.

The winners will be those who simplify claims, explain timelines clearly, and stay accountable after purchase.

Micro And Modular Insurance Will Finally Scale

India’s future workforce will not look like the past. The country already has:

Over 230 million gig and informal workers.

(Source: World Bank, NITI Aayog)

This workforce needs:

Short-term covers

Usage-based pricing

Income and health protection that fits unstable cashflows

Thus, micro-insurance is no longer optional but an essential infrastructure.

Why Platforms Like SMC Insurance Matter Now

In a market full of choice, clarity becomes the differentiator and the role goes beyond selling. It includes:

Honest comparison

Post-sale support

The Road Ahead: Depth Will Define Leadership

Over the next decade, India’s insurance leaders will not be defined by premium volume alone. They will be judged by:

How much the protection gap narrows

How deeply coverage reaches beyond metros

How many claims are settled smoothly

How many first-time buyers stay insured

With strong regulation, rising digital comfort, and platforms focused on real protection, the ecosystem is ready for its next chapter.

Key Takeaways

India’s total insurance penetration declined to 3.7% of GDP in FY2023-24, with life insurance penetration falling to 2.8% and non-life insurance holding near 1.0%, according to the IRDAI Annual Report 2023-24.

Global insurance penetration averages roughly 7%, and advanced economies often exceed 9-11%, leaving India’s insurance depth well below international norms, per Swiss Re Sigma data.

India’s insurance density stood at approximately USD 95 per capita in FY2023-24, compared with a global average exceeding USD 850, according to IRDAI and Swiss Re data.

Urban Indian households show 60-65% insurance coverage, while fewer than 25-30% of rural households are meaningfully insured, per World Bank, NITI Aayog, and IRDAI-backed studies.

India’s insurtech market was valued at USD 0.9 billion in 2024 and is projected to reach USD 11.9 billion by 2033, growing at a CAGR of over 29%, according to IMARC Group.

Embedded insurance models linked to vehicle purchases, credit, and travel can increase first-time insurance adoption by 20-30%, according to Swiss Re Institute research.

India has more than 230 million gig and informal workers who need short-term, usage-based, and income-linked insurance products, per World Bank and NITI Aayog data.

Faster claim settlement and transparency, rather than premium discounts, are now the strongest drivers of policy renewal intent, according to IRDAI.

Frequently Asked Questions

What is the insurance protection gap in India, and how large is it?

The protection gap is the difference between India’s rising insurance premiums and its actual insurance penetration and density. Total insurance penetration fell to 3.7% of GDP in FY2023-24, well below the global average of about 7%, and insurance density stood at roughly USD 95 per capita versus a global average of over USD 850.

Why is rural India so much less insured than urban India?

Urban India has 60-65% household insurance coverage, while fewer than 25-30% of rural households are meaningfully insured. This gap exists because rural and informal households face irregular income, seasonal risk, and higher exposure to health and climate shocks, while most insurance products still assume fixed salaries and long commitments.

How will insurtech and embedded insurance close India’s coverage gap?

India’s insurtech market is projected to grow from USD 0.9 billion in 2024 to USD 11.9 billion by 2033 at a CAGR of over 29%. Embedded insurance models, such as motor cover at vehicle purchase and health cover bundled with credit, can increase first-time adoption by 20-30%, while data-driven underwriting and faster claims settlement are expected to build the trust needed for micro and modular insurance to scale among India’s 230 million gig and informal workers.

Disclaimer: The opinions expressed within this article are the personal opinions of the author. The facts and opinions appearing in the article do not reflect the views of IIA, and IIA does not assume any responsibility or liability for the same.